Original Date

Aug 28, 2025

Reading Time

4 min

Treasury Insight

Modern CFO

Latest Update

Nov 24, 2025

The Hidden Cash Management Crisis: What Mid-Sized Firms Are Missing

In the corridors of mid-sized businesses across the globe, a peculiar contradiction exists. Finance teams meticulously craft budgets, build sophisticated forecasting models, and track dozens of KPIs—yet when it comes to the cash sitting in their bank accounts, they operate in a strategic void.

This isn't just an oversight. It's a costly blind spot that's quietly eroding returns and exposing businesses to unnecessary risk.

The Great Cash Management Paradox

Picture this: Your finance team has KPIs for everything from accounts receivable turnover to inventory management, from capital expenditure efficiency to working capital optimization. But ask them about their cash optimization metrics, and you'll likely be met with blank stares.

Here's the uncomfortable truth: Most mid-sized firms treat cash management like a necessary evil rather than a strategic opportunity. They forecast it, monitor it, and then... let it sit. Often earning minimal returns while inflation quietly chips away at its value.

This gap between planning and execution isn't just an operational hiccup—it's a fundamental disconnect that reveals how finance teams are leaving money on the table, sometimes literally millions of dollars annually.

Why CFOs Are Avoiding Treasury

(And Why That's Changing)

There's an old saying in finance circles: "Treasury is all risk, no reward." Many CFOs and controllers have historically viewed cash management as a minefield of compliance issues and interest rate risks, preferring to keep things simple with basic checking accounts and minimal yields.

But the landscape has shifted dramatically. According to PwC's latest survey of leading companies, cash and liquidity management now ranks as the #2 priority for CFOs and the #1 priority for treasurers. The message is clear: cash optimization is no longer optional—it's essential.

The modern CFO who ignores treasury management isn't being prudent; they're being negligent.

🪄Where the Real Magic Happens

(And Where Most Companies Stop)

Traditional cash management follows a predictable pattern: consolidate information from various systems, track cash flows from receivables and payables, monitor capital expenditures, and measure everything against current liquidity. It's methodical, it's thorough, and it stops right where the real opportunity begins.

The moment cash hits the bank account is precisely when strategic cash management should kick into high gear.

Yet for most mid-sized firms with lean finance teams, this is where the process ends. Cash sits in low-yield accounts, earning returns that barely keep pace with inflation, while opportunities for optimization go unexplored.

With the right approach and tools, organizations can transform this endpoint into a value creation engine—enhancing yields, automating processes, ensuring compliance, and strategically diversifying banking relationships for better risk management.

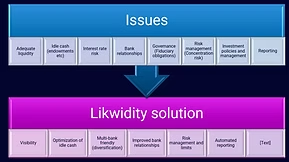

❓The Questions Every Finance Leader Should Be Asking (But Most Aren't)

If you're responsible for your organization's financial health, these questions should keep you up at night:

- Where should we invest our cash? Beyond the basic checking account, what options exist?

- Which bank is paying the best interest? Are you comparing rates across your banking relationships?

- What is the credit rating of the banks we deal with? Are you inadvertently concentrating risk?

- How much should we invest per bank? What's your diversification strategy?

- How long should we invest our funds for? What's the optimal balance between yield and liquidity?

- Can we access our funds when needed? What are the terms and penalties?

- What's the difference between bank deposits and money market funds? Which serves your needs better?

- What happens when investments mature? Do you have an automated reinvestment strategy?

- What is cash optimization, and does it actually matter? (Spoiler: It matters more than you think.)

If you can't answer these questions confidently, you're not alone—but you are missing opportunities.

The Cost of Inaction: What Mid-Sized Firms Are Losing

Consider a mid-sized firm with $10 million in average cash holdings. The difference between a basic checking account (earning 0.1%) and optimized cash management (earning 4-5%) isn't just a few basis points—it's potentially $400,000+ in annual returns.

Multiply this across thousands of mid-sized firms, and we're talking about billions of dollars in lost opportunity annually. Money that could fund growth initiatives, improve cash flow resilience, or simply enhance shareholder returns.

📢Introducing Automated Cash Optimization

The solution isn't hiring a treasury team or implementing a complex Treasury Management System (TMS). Modern cash optimization requires modern tools—solutions that can bridge the gap between sophisticated planning and practical execution.

Automated Cash Optimization

Likwidity is a straightforward tool that automates complex cash management processes without expensive implementations.

Our dashboard provides real-time visibility into interest earned, funds allocation, credit rating distribution, maturity profiles, and bank limit utilization.

You can reach our customer support team by emailing info@yourcompany.example.com, calling +1 555-555-5556, or using the live chat on our website. Our dedicated team is available 24/7 to assist with any inquiries or issues.

We’re committed to providing prompt and effective solutions to ensure your satisfaction.

We offer a 30-day return policy for all products. Items must be in their original condition, unused, and include the receipt or proof of purchase. Refunds are processed within 5-7 business days of receiving the returned item.

- Real-time rate notifications from each banking partner

- Automated interest calculations for accurate forecasting

- Maturity notifications with rollover or withdrawal options

- Comprehensive audit trails for compliance and governance

- Early withdrawal coordination when liquidity needs change

- Rate negotiation tools to optimize pricing with banks

Our Commitment: Transparency and Control

Likwidity operates on three core principles:

- Pure software tool: We charge a fixed monthly fee with no hidden commissions, rebates, or markups. You receive the full quoted rate from your banks.

- Non-intrusive partner: We don't interpose between you and your banking relationships. You maintain full control and direct engagement with your relationship managers.

- Zero access to funds: We never receive, access, or control your cash or bank accounts. Think of us as a sophisticated plugin that connects your accounting/ERP/treasury systems.

🚀The Future of Cash Management

Reliability

Forward-thinking CFOs are recognizing that letting cash sit idle is no longer conservative management—it's value destruction.

Financial Optimization

Mid-sized firms can now automate cash management processes while maintaining the full control and oversight that finance leaders demand.

Automated Efficiency

The magic that should happen when cash hits your bank account is now measurable, automatable, and readily available for your business.

Scalability

Discover how to bridge your cash management gap and start optimizing returns while maintaining full control over your banking relationships.

Recent Posts

Stay updated with our latest industry insights and expert corporate cash management advice.

Mastering Corporate Cash Optimization with Likwidity

Learn how Likwidity helps organizations streamline their cash flow processes and improve overall financial efficiency.

Issues around cash management for schools

Explore the unique financial challenges that educational institutions face and how effective management strategies can help.

Master Guide on what firms should do with idle or surplus cash funds

A comprehensive resource for businesses looking to put their surplus cash to work for better returns and stability.

Comments

Loading…