Publication Date

Dec 4, 2025

Reading Time

4 min

Topic Analysis

Assets

Last Updated

Dec 8, 2025

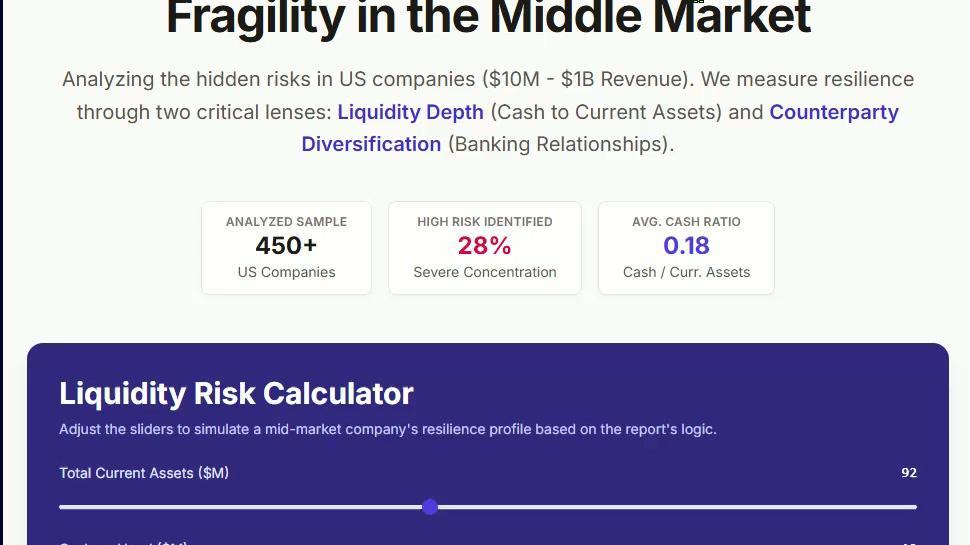

Research consistently show that a low cash-to-working-capital ratio is not just a liquidity red flag—it directly correlates with reduced operational flexibility, higher financing costs, and compressed margins, especially during economic stress. Firms that actively manage this ratio—neither hoarding nor depleting cash—tend to exhibit more stable and resilient profitability.

Liquidity risk management

Cash to Total assets

- Shoe Industry 12

- Cash Millions $11,129

- Cash/Firm Value 6.11%

- Cash/Revenues 15.63%

- Cash/Total Assets 18.95%

- Semiconductor Equip 30

- Cash Millions $21,795

- Apparel Industry 37

- Cash Millions $11,679

- Cash/Total Assets 15.48%

Industry Analysis Overview

Comparative metrics across diverse sectors showing growth potential and key financial performance indicators.

Retail (Grocery & Food)

Retail sectors showing steady growth with 17 key players influencing current market dynamics.

View Details- Growth rate at 10.74%

- Market margin 5.95%

- Profit ratio 14.33%

- Stable performance

Coal & Energy

Energy sector analysis including 16 distinct companies navigating current market shifts.

View Details- Growth rate at 12.87%

- Market margin 23.15%

- Profit ratio 14.21%

- High demand index

Biotech Drugs

Biotechnology research involving 535 firms pushing the boundaries of medical innovation.

View Details- Growth rate at 5.07%

- Market margin 36.27%

- Profit ratio 12.91%

- R&D heavy sector

Industry Performance Metrics

- Real Estate (Operations & Services) 60

- Hotel/Gaming 65

- Advertising 54

- Homebuilding 30

- Electronics (General) 122

- Telecom. Equipment 61

- Software (Internet) 29

- Market Capitalization $23,270.49

- Average Returns 11.33%

- Industry Volatility 10.63%

Software Sector

Entertainment

Company Count

81

Average Cash

$75,788.19

Cash to Assets

1.88%

Cash to Sales

14.11%

Cash to Market

10.06%

Banking Failures Summary

- 2025 Bank Failures (YTD) 1

- 2024 Bank Failures 2

- 2023 Bank Failures 5

- 2022 Bank Failures 3

- 2021 Bank Failures 0

- 2020 Bank Failures 4

- 2019 Bank Failures 4

- 2018 Bank Failures 4

- 2017 Bank Failures 8

- 2016 Bank Failures 5

Academic finance research consistently identifies a low cash-to-working-capital (CWC) ratio as a significant indicator of financial vulnerability and operational risk for firms. The cash-to-working-capital ratio—typically defined as (Cash + Cash Equivalents) ÷ (Current Assets – Current Liabilities)—measures the proportion of a firm’s net working capital that is held in highly liquid form. A low ratio suggests limited liquid buffers relative to short-term operational needs, which can have several adverse implications:

1. Almeida, H., Campello, M., & Weisbach, M. S. (2004).

“The Cash Flow Sensitivity of Cash.”

Journal of Finance, 59(4), 1777–1804.

https://doi.org/10.1111/j.1540-6261.2004.00674.x

- Key Insight: Introduces the idea that financially constrained firms (often with low liquidity) exhibit higher sensitivity of cash holdings to cash flows—highlighting their inability to smooth operations during downturns, which can pressure margins.

2. Bates, T. W., Kahle, K. M., & Stulz, R. M. (2009).

“Why Do U.S. Firms Hold So Much More Cash Than They Used To?”

Journal of Finance, 64(5), 1985–2021.

https://doi.org/10.1111/j.1540-6261.2009.01492.x

- Key Insight: Documents a secular rise in corporate cash holdings; firms with low cash buffers are shown to be more vulnerable during crises, often cutting investment and R&D—actions that can reduce future margins.

3. Acharya, V. V., Almeida, H., & Faure-Grimaud, A. (2007).

“The Illiquidity of Corporate Bonds.”

NYU Working Paper (also published in later forms in top journals).

- While focused on bond markets, this line of work (including related papers by the authors) shows how firms with weak balance sheets (including low liquid assets relative to short-term needs) face higher external financing costs, compressing net margins.

4. García-Teruel, P. J., & Martínez-Solano, P. (2007).

“Effects of Working Capital Management on SME Profitability.”

International Journal of Managerial Finance, 3(2), 164–177.

https://doi.org/10.1108/17439130710738762

- Key Insight: Finds a strong negative relationship between aggressive working capital management (e.g., very low cash, high receivables days) and firm profitability—suggesting margin damage from insufficient liquidity.

5. Opler, T., Pinkowitz, L., Stulz, R. M., & Williamson, R. (1999).

“The Determinants and Implications of Corporate Cash Holdings.”

Journal of Financial Economics, 52(1), 3–46.

https://doi.org/10.1016/S0304-405X(99)00003-6

- Key Insight: Shows that firms with low cash holdings relative to operational needs tend to have higher leverage, lower profitability, and greater investment-cash flow sensitivity—indicating margin vulnerability.

Recent Empirical Studies

Linking Liquidity, Working Capital, and Margins for optimal financial performance.

Azim & Islam (2020)

Working Capital Management and Firm Profitability: Evidence from Australia.

Journal of Applied Accounting

Full research findings on capital efficiency.

Ding, He, & Li (2022)

Liquidity Management and Corporate Investment Efficiency in modern markets.

Journal of Corporate Finance

Detailed analysis of corporate finance and investment.

Key Findings Summary

Firms with low liquidity underinvest during downturns, impacting long-term growth.

Moody’s Analysis

Assessing corporate liquidity resilience and stress testing during post-pandemic market conditions.

IMF Global Reports

Evaluating corporate debt and liquidity buffers within higher interest rate economic environments.

S&P Intelligence

Analyzing cross-sector working capital trends and their impact on corporate EBITDA margins.

Practitioner Insight

A balanced cash-to-working-capital ratio is critical for maintaining profitability and operational resilience.

Recent Posts

See All

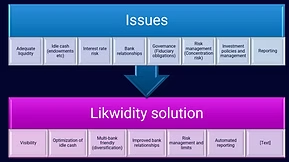

Mastering Corporate Cash Optimization with Likwidity

Optimize your company's idle cash flow and maximize returns with our strategic financial tools designed for modern corporate needs.

Issues around cash management for schools

Navigating the unique financial complexities and treasury management challenges that educational institutions face in today's economy.

Master Guide on what firms should do with idle or surplus cash funds

Discover essential strategies and best practices for managing your firm's surplus capital to ensure long-term stability and growth.